Skies are darkening, headwinds are emerging and the water is growing quite choppy for the U.S. office sector. Stubbornly low physical occupancy and a decelerating economy will place downward pressure on the sector this year and likely the next few years as well.

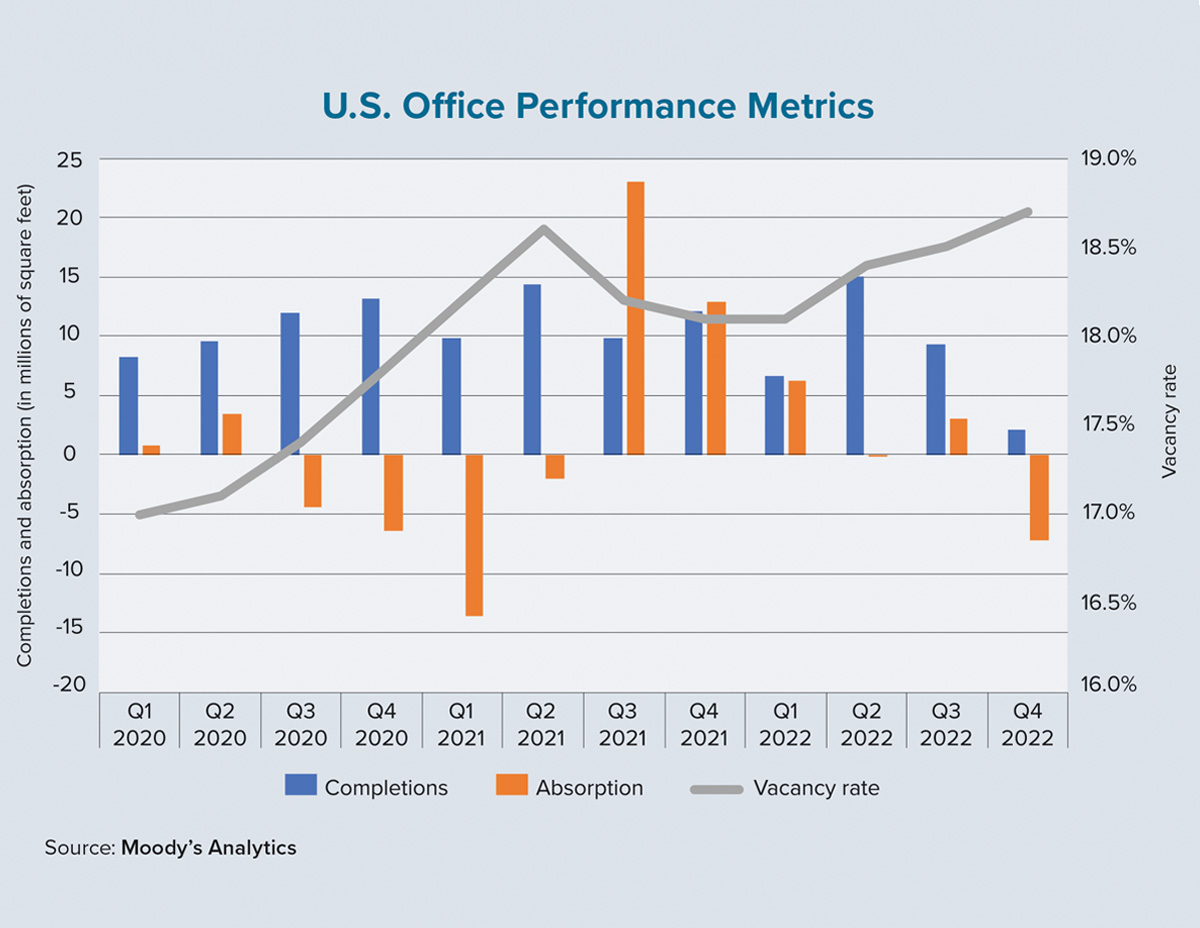

Even before the calendar flipped to 2023, office performance metrics had deteriorated. The national vacancy rate increased by 60 basis points during the course of 2022 and the year-end rate of 18.7% was a pandemic-era high. Furthermore, the record-high vacancy rate of 19.3% (last observed in 1991 in the wake of the savings and loan crisis) is now within striking distance.

Layoffs across office-using companies continue to be a concern. Downsizing by Salesforce, Twitter and Amazon, among many others, have populated headlines for months. Interestingly, however, these headline-inducing layoffs may be misleading in terms of office real estate. Current labor market dynamics may actually make CEOs reluctant to significantly reduce their workforce as a way to manage profit margins in this softening economy. Instead, reducing the amount of office space may be more palatable.

While real estate tends to be a small share of the corporate cost structure, the potential to use hybrid and remote work (even temporarily) makes some office space expendable. For business executives who were already unsure of their long-term office-space needs, any leases expiring in the near future are prime candidates for nonrenewal or significant renegotiation.

The coming troubles in the office sector will be particularly apparent for Class B/C properties in urban areas. As leases expire and tenants opt for space reductions, it is likely that the number of vacancies across existing properties, along with any new inventory, will prompt decisionmakers to consider higher-quality and better-located spaces. Savings from reduced space, combined with likely concessions from property owners, may make this an ideal time for an upgrade. This situation in no way makes urban Class A offices immune to trouble. The recent news of difficulty for two prominent properties in downtown Los Angeles, along with continued woes in Midtown Manhattan, shows the breadth of the struggles within the sector.

This year will be particularly telling in terms of the longer-term sentiment for office investors. Following the Great Recession, 2013 was a rebound year for capital-markets activity. An upcoming “wall of maturities” that includes many relatively low-debt-yield loans will make refinancing difficult in today’s interest rate environment. A good deal of additional equity will need to be offered by market participants to make any refinance or purchase transaction push through. There is plenty of dry powder ready to deploy into commercial real estate, but it remains to be seen whether the office sector will be a main recipient.

No matter the angle taken, it is clear that the office sector is going to be tested in the next couple of years. Reaching a new equilibrium will likely require some rightsizing of the market. This will necessitate the repurposing of certain properties, and it is likely that some traditional office clusters in certain metro areas will be forced to rezone toward mixed use. But this is not necessarily a negative for the long-term future of these neighborhoods.

Finally, the next few years are unlikely to result in an apocalyptic situation for the sector. Yes, there are many challenges, but there are also opportunities to revamp the office stock while creating better, healthier spaces for workers and urban residents alike. Physical occupancy may never return to its pre-pandemic levels, but as office spaces and locations improve, positive sentiment regarding the usefulness of in-person interaction will return.

The combination of a more flexible workplace and better work environments may usher in a new era of productivity, which would ultimately be a boon for office-space needs. In fact, Moody’s Analytics models show that occupancy rates will improve starting in 2024. Without sounding overly optimistic, offices will remain an integral part of society and a new equilibrium will emerge, but some dark skies and choppy waters must be traversed to get there. ●