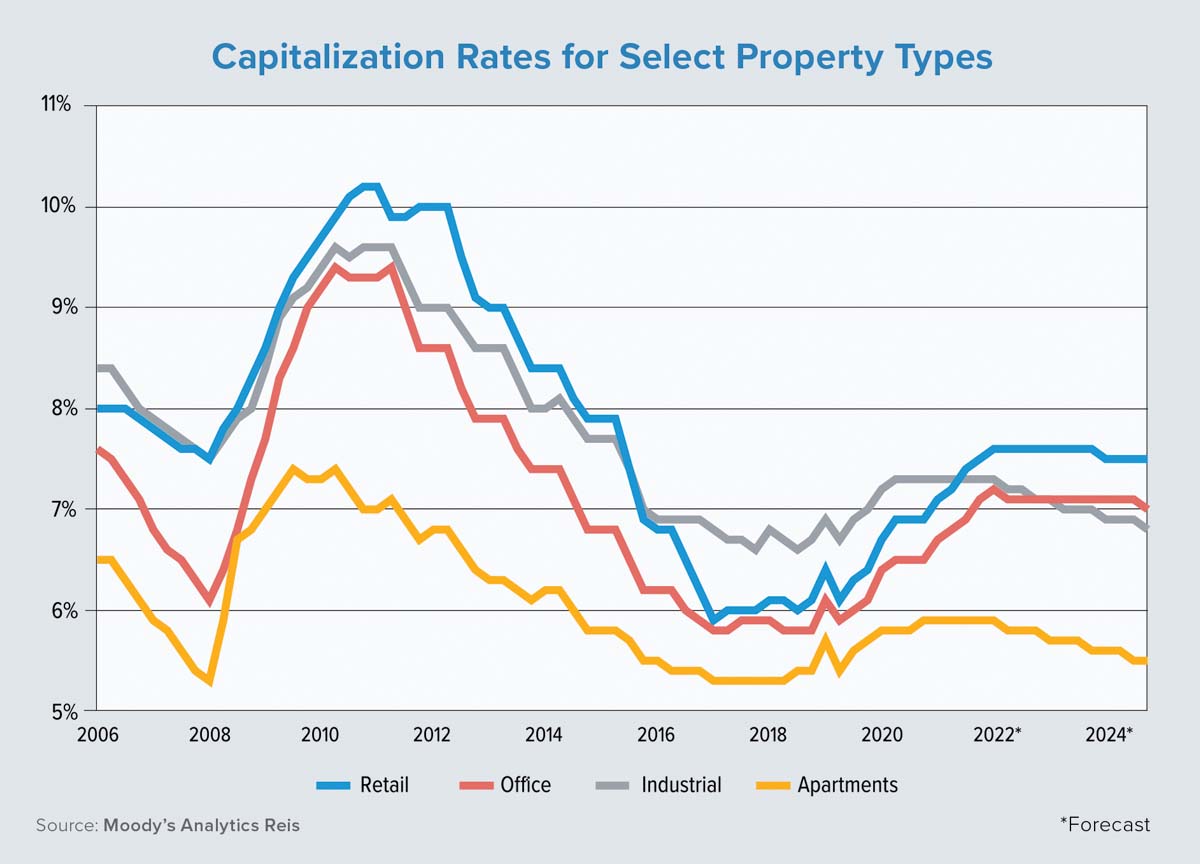

The past year was a strong one for U.S. commercial real estate and the domestic economy. Early concerns for the commercial mortgage industry largely proved unwarranted given the more recent flurry of positive data. Stabilization in the office and retail sectors, combined with soaring performances for multifamily and industrial assets, have once again illustrated the resilience and value of commercial real estate for investors.

As for the coming year, there are a few emerging headwinds, but overall fundamentals are strong. This is prompting industry stakeholders to exude a generally bullish tone when analyzing the prospects for commercial real estate success. So, where has the market been and where is it going?

The general sentiment in early 2021 was one of concern. Other than the warehouse and distribution sector, which had a solid 2020 on the back of growth in e-commerce, there tended to be more questions than answers in regard to the potential performance of commercial real estate. What will be the true shape of the economic recovery? Will jobs return sufficiently to boost income and household formations? Do shoppers care about the brick-and-mortar experience? How much will office-using companies reduce their square footage in a new era of remote work?

While we do not yet have the full answer to the office-space question, concerns of a tepid recovery from the COVID-19 pandemic have mostly gone by the wayside. Gross domestic product (GDP) is expected to grow by 6% this year. The unemployment rate dropped below 5% and while some individuals are showing reluctance to return to the labor force, those who want work can get it — and often at a higher level of compensation than before.

Along with generous fiscal stimulus by the federal government, this has boosted household formations and served as a boon for retail spending. In third-quarter 2021, retail sales volume was up 13% year over year, according to census figures. Overall, the U.S. economy in 2021 was quite robust.

Data from the last six months of 2021 illustrates a substantial improvement in space-market performance compared to 2020 and even the first half of 2021. As shown by plummeting vacancy rates and swelling effective-rent levels, multifamily and industrial properties each had a banner year. U.S. multifamily effective rents increased by a whopping 7.9% from Q2 to Q3. Amazingly, this quarterly record more than tripled the previous high mark for a statistic that Moody’s Analytics Reis has tracked since 1999.

With this exceptional quarter in the books, we now expect full-year 2021 growth for multifamily rents to hit double digits. What is the economic rationale for this growth? Demand has been incredibly strong as nearly 95,000 apartment units were absorbed in Q3 alone. While this dwarfed the recent quarterly average of about 50,000 units, it is not a record as 133,000 units were absorbed in Q1 2019.

Household formations and demand for apartments have not been the only factors in this astounding performance. Higher wages and excess savings from government stimulus efforts have prompted some households to upgrade their standard of living. This phenomenon of increased interest in larger, more amenity-filled apartments has somewhat skewed demand toward higher-priced properties. Additionally, general inflationary pressures for the economy and a growing affordability problem for single-family homes are playing a role.

Among the U.S. multifamily markets with the highest rent-growth rates, Phoenix topped the list in Q3 2021 with a year-over-year surge of 22.9%. It was followed closely by Tucson, Arizona; Tampa-St. Petersburg, Florida; and Albuquerque, New Mexico. Our data also has seen consistently strong demand in mid-tier cities in the Mountain West and South Atlantic regions.

The industrial real estate sector, particularly warehouse and distribution properties, also realized a record performance. Rent levels are above average, but the astounding 310-basis- point decrease in the vacancy rate over the first three quarters of 2021 is what truly grabbed our attention. About two-thirds of this decline occurred in Q3 alone.

Solid retail performance combined with the expectation of continued growth in e-commerce (which generally requires more warehousing space) is fueling this trend. But there’s also a noteworthy shift in the approach of manufacturers and retailers toward “just-in-case” inventory strategies. This began to take shape early in the pandemic given a lack of necessities on store shelves, but it has continued due to supply chain issues that have emerged into greater focus over the past six months.

While the office and retail sectors haven’t broken any records, these two asset classes have done quite well relative to prior expectations. Even before the pandemic, retail- and office-sector performance was less than stellar. Vacancy rates were increasing and rent growth was muted. E-commerce had already put a dent in the strength of brick-and-mortar retail while speculative supply had limited the potential of office performance.

When the pandemic hit, speculation was rampant regarding how well these sectors would handle the immediate repercussions and the long-term structural changes. Today, nearly two years after the start of the pandemic in the U.S., we find that the stress has not (and likely will not) materialize in any systematic way.

In fact, for retail in particular, “turned the corner” is an apt description. The U.S. retail vacancy rate declined in Q2 and Q3 2021. Effective rent growth returned to positive territory in Q3 and early Q4 data indicated that this will continue. While this is wonderful news for a sector that had repeatedly thrown around the word “apocalypse,” there is still likely to be idiosyncratic stress that is mainly reserved for Class B and C properties in locations that tend to have stagnating or declining population growth.

From the office perspective, space-market performance has been similarly positive. After subtle rent-growth declines were recorded in Q1 2021, rent levels have stabilized. The vacancy rate dropped by 30 basis points from its pandemic-era high and stood at 18.2% as of Q3. Is the office sector completely out of the woods? Likely not, as many companies may still reduce their real estate holdings as remote- and hybrid-work plans take shape, but a large-scale fallout from the pandemic has yet to materialize.

In general, commercial real estate is in a good position. Fundamentals are strong and the macroeconomy is on track to have another above-average year. GDP and employment growth should continue in earnest. Furthermore, development- and capital-market participants have continued to act with restraint. In fact, part of the strength shown by the industry throughout the pandemic is due to the excellent pre-pandemic lending standards.

This has allowed lenders, owners and tenants to better work together and provide stability to the market during the worst of times. And it has allowed these parties to better take advantage of the reopening economy and subsequent recovery. In the same vein, developers acted slowly in terms of supply growth, which also helped to maintain this stability. While this pipeline is now growing and we are forecasting a strong 2022 in terms of completions, absorption across all major asset classes should be sufficient to promote further rent growth in the new year.

None of this is to say that headwinds are absent. We continue to closely monitor supply chain issues and inflation. And while the direct effects of these economic phenomena on commercial real estate are somewhat minimal, impacts on particular industries or macroeconomic health could prove indirectly concerning for commercial mortgage brokers and lenders. The Moody’s Analytics Supply Chain Stress Index rose throughout the second half of last year, illustrating difficulties in the labor market and the transportation sector. As noted, however, the direct effects on commercial real estate finance have actually tended to be positive.

Out of concern for shortages, retailers continue to utilize emergency inventory strategies, which will mean further growth for the warehousing and distribution sector. We expect industrial rent growth to exceed 4% in 2022. Conversely, we recognize difficulties for some manufacturers and large multinational firms that rely on a well-functioning global supply chain network. In areas such as Chicago and the Greater Midwest, which have clusters of these businesses, long-term supply chain issues could reverberate and slow down the post-pandemic recovery.

What else are we watching in 2022? In the past, strong economic and real estate performance would promote an uptick in speculative supply. Currently, our surveys indicate a strong pipeline of development projects in the early and middle stages — especially for multifamily and industrial. While these two sectors are the most likely to succeed in absorbing any completions, setbacks in demand will place pressure on their space-market performance.

As for retail and office properties, development is likely to remain modest and new projects will be mainly located in major metros with high population growth. We also are closely monitoring business travel as it relates to lodging and urban retail. Transportation Security Administration data shows that air travel has remained strong even during the spread of the delta variant and the typical post-summer decline in leisure travel. This is a subtle indicator that the forecast of a large-scale and long-lasting reduction in business travel may be unfounded.

Lastly, the commercial real estate industry seemed to become quite aware of climate risk in 2021. The increasing frequency of wildfires and floods, combined with more legislative efforts related to climate change, have prompted an increase in webinars and conferences devoted to this topic. With the potential for more acute events and more stringent regulations on the horizon, we think 2022 is the year when commercial real estate stakeholders move from discussing the issues to initiating deeper levels of modeling, forecasting and planning for how climate change will impact their assets and the industry as a whole. ●